Many businesses fail because of cash flow problems. When cash flow is tight, companies often need to turn to creative financial solutions.

While a traditional business loan used to be one of the few options, now companies looking to improve cash flow can compare accounts receivable financing vs. factoring to find the best solution. But which option is right for your company?

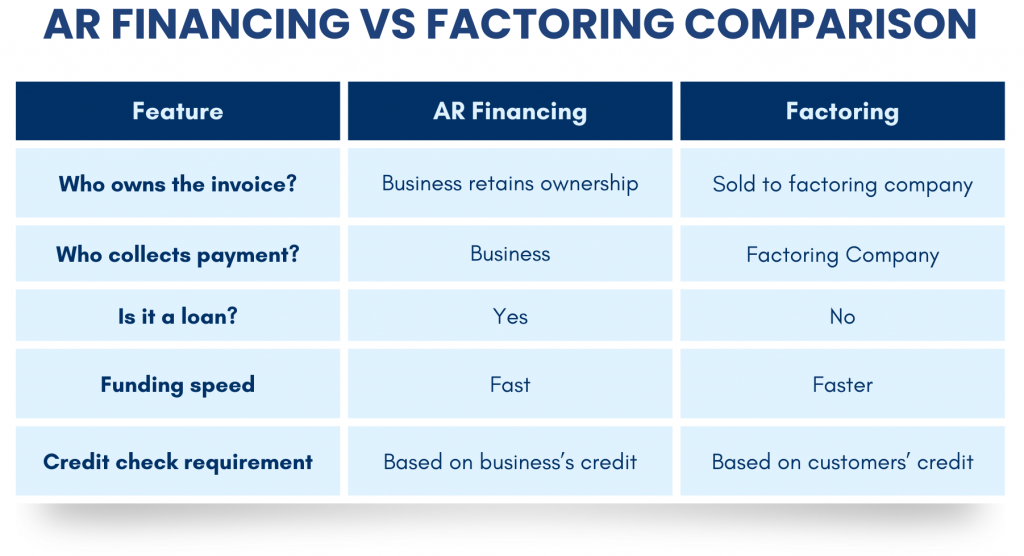

Both options help businesses turn unpaid invoices into working capital, but they work differently and suit different business needs. Understanding their key differences can help you choose the best option for your company.

What Is Accounts Receivable Financing?

Accounts receivable financing (AR financing) is a type of loan where a business uses its unpaid invoices as collateral to secure funding. Rather than selling invoices, the company borrows against them, receiving a percentage of their value upfront. Once customers pay their invoices, the business repays the lender, plus interest and fees.

Key Features:

- Business keeps ownership and control over invoices.

- Customers continue paying to the business directly.

- The company repays the loan with interest. Often deducted directly from your business checking account.

This option is particularly useful for companies that want to maintain strong customer relationships and have financial stability to handle structured repayments.

How Does Accounts Receivable Financing Work?

Accounts receivable financing is easier to understand when you see it in action. Here’s a step-by-step process of how it works:

Step 1: Apply for AR Financing.

The business submits an application to a financing provider, along with details of its outstanding invoices. The lender evaluates the company’s creditworthiness and financial stability.

Step 2: Receive an Advance.

Once approved, the lender provides a cash advance, typically 70-90% of the invoice value. The business continues to own and manage the invoices.

Step 3: Customer Pays the Business.

Customers make payments directly to the business according to their normal terms. The business is still responsible for following up on payments.

Step 4: Repay the Loan.

After collecting payments from customers, the business repays the lender the full amount advanced, plus interest and any agreed-upon fees. Typically repayment is deducted directly from the business checking account.

Step 5: Access Additional Financing as Needed.

As new invoices are generated, businesses can continue using AR financing to maintain steady cash flow.

What Is Factoring?

Factoring, also known as invoice factoring, involves selling unpaid invoices to a factoring company at a discount. A factoring company, like Riviera Finance, advances a large portion of the invoice value up front and then collects payments directly from customers. Once the customers pay, the business receives the remaining balance, minus the factoring company’s fee.

Key Features:

- The business sells invoices to a third party, the factoring company.

- The factoring company collects payments directly from customers.

- No loan repayment because funding is based on invoice sales.

Factoring can be an excellent choice for businesses that need immediate cash flow without taking on additional debt. Get an in-depth look at factoring in our Factoring Costs and Benefits article.

How Does Factoring Work?

Let’s look at an overall picture of factoring to give you a better understanding of how it works.

Step 1: Sell Invoices to a Factoring Company.

The business submits its outstanding invoices to a factoring provider. The factoring company assesses the creditworthiness of the business’s customers (not the business itself).

Step 2: Receive an Advance Payment.

The factoring company advances a percentage of the invoice value, usually 80-95%, providing immediate cash flow.

Step 3: Factoring Company Collects Payment.

Instead of paying the business, customers send their payments directly to the factoring company. The factoring company manages collections, which can reduce administrative burdens.

Step 4: Receive Remaining Balance Minus Fees.

Once the customer pays in full, the factoring company releases the remaining balance to the business, minus its factoring fee (typically 1-5% of the invoice value).

Step 5: Repeat as Needed.

Businesses can continue selling invoices to maintain cash flow without taking on debt.

Key Differences Between Accounts Receivable Financing and Factoring

When looking at AR financing vs. factoring, it’s important to understand the main differences between the two. Here’s a side-by-side comparison:

Pros and Cons of Accounts Receivable Financing vs. Invoice Factoring

When choosing between accounts receivable financing and factoring, it’s essential to weigh the benefits and drawbacks of each. Both methods can improve cash flow, but they come with different costs, risks, and impacts on customer relationships.

Accounts Receivable Financing Pros:

- Retain control over customer relationships: Your clients continue to pay you directly, maintaining trust and consistency.

- Flexible funding based on invoices: Access working capital without giving up ownership of receivables.

- Good for businesses with strong credit: Companies with solid financials can secure better terms and lower interest rates.

Accounts Receivable Financing Cons:

- Requires repayment with interest: Since it’s a loan, you’ll need to repay the amount borrowed, plus fees and interest.

- More difficult for new businesses and businesses with poor credit: Lenders evaluate your business’s creditworthiness, which can be a barrier to approval.

- Repayment is often facilitated by direct withdrawal from the business checking account. If insufficient funds are available this can lead to penalties and/or payment issues for other expenses.

Factoring Pros:

- Immediate cash flow boost: Get funds quickly without waiting for customers to pay.

- No debt or loan repayment: Since invoices are sold, there’s no obligation to pay back a loan.

- Supports business growth and scaling: Invest in staff, inventory, and operations without waiting on slow-paying customers. Unlike loans with fixed payments, factoring scales with your sales.

- Easier approval based on customer creditworthiness: Factoring companies focus on your customers’ ability to pay, not just your business’s credit history.

Factoring Cons:

- All invoices may not be approved for factoring: In order to factor an invoice, the factoring company needs to be able to credit approve the customer and verify the invoice.

- May have higher fees compared to traditional loans: Factoring fees are often higher, because of the additional services provided.

Read testimonials from real business owners on how factoring has helped their business.

Real World Examples: How Businesses Use AR Financing and Factoring

To better understand how account receivable financing and factoring work in practice, let’s explore two businesses that used these methods to manage their cash flow effectively.

Case Study #1: A Marketing Agency Uses Accounts Receivable Financing to Maintain Operations

The Challenge:

Great Ideas Marketing, a mid-sized digital marketing agency, had several large corporate clients who regularly delayed payments for 60–90 days. While the agency had strong revenue, cash flow shortages made it difficult to cover payroll, invest in new software, and hire additional staff. The company needed a way to bridge the gap without giving up control of its accounts receivable collections.

The Solution:

Instead of taking out a traditional business loan, Great Ideas Marketing opted for accounts receivable financing. The agency used its open accounts receivable as collateral to secure a loan from a lender, receiving 90% of the invoice value upfront. Once their clients paid, the company repaid the loan plus interest and fees.

The Result:

With predictable cash flow, Great Ideas Marketing was able to:

- Continue paying employees on time.

- Invest in new marketing tools to scale operations.

- Maintain direct relationships with clients without a third party collecting payments.

Case Study #2: A Trucking Company Uses Factoring to Keep Trucks Moving

The Challenge:

FastLane Freight, a small trucking company, often faced long delays in receiving payments from clients, with invoices taking up to 60 days to be paid. Meanwhile, the company needed immediate cash to cover fuel, truck maintenance, and driver salaries. Waiting for payments wasn’t an option, and securing a loan was difficult due to fluctuating revenue.

The Solution:

FastLane Freight decided to use invoice factoring. They sold their outstanding invoices to a factoring company, which provided 95% of the invoice value upfront. The factoring company then collected payments directly from customers.

The Result:

By using factoring, FastLane Freight was able to:

- Receive immediate cash to keep trucks running and deliveries on schedule.

- Avoid taking on additional debt or worrying about repayment.

These two case studies highlight how businesses can use accounts receivable financing or factoring based on their specific cash flow challenges. While both options provide immediate working capital, the right choice depends on factors like a business’s credit, customer payment cycles, and how much control a business wants to maintain.

Which Option Is Best for Your Business?

Choosing between receivables financing vs. factoring depends on several factors, including your business’s financial health, industry, and how much control you want to maintain over customer payments.

Choose account receivable financing if:

- You want to keep strong customer relationships without third-party involvement.

- Your business has good credit and qualifies for favorable loan terms.

- You prefer structured repayments over selling invoices outright.

Choose factoring if:

- You need quick access to cash without taking out debt.

- Your customers have strong credit histories, making invoice sales easier.

- You’re an industry with slower-paying clients, like trucking, staffing, or manufacturing.

Get the Cash Flow Your Business Needs with Riviera Finance

Riviera Finance is ready to be your business financing partner. We are experts in accounts receivable management, cash flow solutions, and invoice factoring solutions. As a nationally recognized leader in business financing and over 56 years of experience, you can trust us with your cash flow needs.

Explore your financing options today with Riviera Finance. Contact us today to find the best solution for your business!