What’s The Difference Between Recourse vs. Nonrecourse Factoring?

Invoice factoring is one of the most reliable ways to speed up payments and grow your business. The difference between recourse vs. nonrecourse factoring is an important distinction you should consider before committing.

Riviera Finance has been providing invoice factoring for small businesses since 1969. When a single late invoice can make you miss payroll or skip over important projects, we want to offer you an alternative. Let’s take a look at the benefits of different factoring types and the impact they can leave on your business.

What Is Invoice Factoring and How Does It Work?

Before we dive into the key differences between recourse and nonrecourse, let’s review what invoice factoring is. This useful service lets you sell your unpaid invoices to a third-party invoice factoring service at a small discount.

Constant missed invoices make it difficult to pay employees, purchase necessary equipment, or partner with other brands. Invoice factoring shortens wait times that can slow down your business and cost you future opportunities. Businesses across many different industries, from hospitality to transportation, depend on invoice factoring to run smoothly.

Want to learn more about invoice factoring? Reach out to our team today, and we’ll be happy to discuss the benefits for your business.

What Is Recourse Factoring vs. Nonrecourse Factoring?

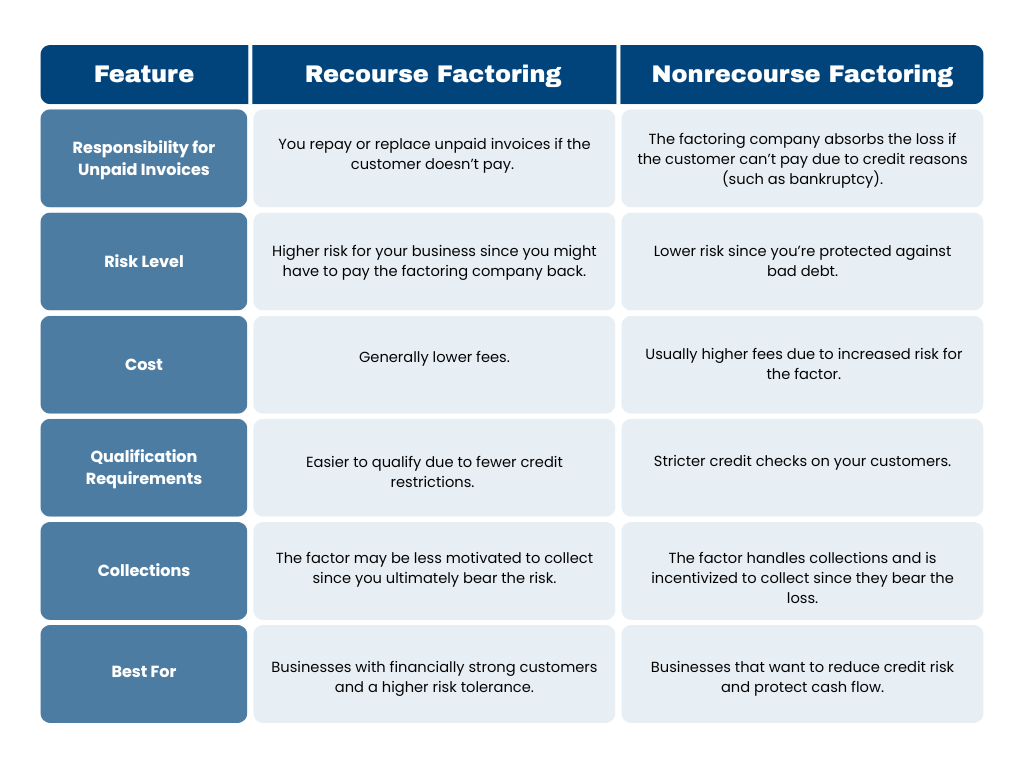

Once you’ve decided to try invoice factoring, you’ll need to consider which kind will suit your business best. Recourse invoice factoring means you’re responsible for buying back your invoice if a customer doesn’t pay the factoring company within a certain amount of time (usually 90 days).

Nonrecourse invoice factoring is the opposite and takes on the risk of nonpayment from clients, offering you more protection. If your customer doesn’t pay what they owe, you don’t have to reimburse a nonrecourse factoring company.

Recourse Invoice Factoring Benefits

- Often lower fees than nonrecourse invoice factoring

- Easy for small businesses to qualify for

- Still performs credit checks on customers to avoid defaults

Recourse Invoice Factoring Drawbacks

- No debt protection if your client doesn’t pay back the invoice

- Recourse invoice factoring companies are less likely to spend resources to collect unpaid invoices

- Credit checks may still not be as rigorous as nonrecourse factoring companies

Nonrecourse Invoice Factoring Benefits

- You don’t need to spend time and resources collecting your unpaid invoices

- The nonrecourse invoice factoring company takes on all the credit risk

- More reliable cash flow due to a more rigorous collection process

Nonrecourse Invoice Factoring Drawbacks

- Cost is a little higher than recourse invoice factoring

- Not as easy to qualify for

Which Type of Invoice Factoring Works Best For You?

Not sure which kind of invoice factoring will help you steady your cash flow and give you peace of mind? Take a look at the table below to review the key differences between recourse vs. nonrecourse factoring.

Frequently Asked Questions

Why is nonrecourse factoring more expensive?

It typically costs more than recourse invoice factoring because the factoring company takes on the risk of customer non-payment. The higher fees reflect the added protection against bad debt.

What types of invoices qualify for nonrecourse factoring?

Invoices typically qualify if they are issued to creditworthy customers with strong payment histories. Factoring companies generally prefer invoices that are for completed, undisputed work or already delivered goods to reduce the risk of non-payment.

What is an example of recourse factoring?

With recourse factoring, if your customer doesn’t pay the invoice within the agreed time, you must buy it back or replace it with another invoice. For example, if you sell a $10,000 invoice to the factor and your client defaults, you are responsible for repaying that $10,000 to the factoring company.

What is an example of nonrecourse factoring?

If you sell a $10,000 invoice to the factoring company and your customer goes bankrupt, you don’t have to repay the amount. The factoring company absorbs the loss, protecting your business from bad debt and lost time.

Get Financial Help With Riviera Finance

You have better things to do than wait on customers to pay what they owe. With Riviera Finance in your corner, you can finally start pouring your energy into starting new projects or forming new business partnerships.

We’re a nonrecourse invoice factoring company that purchases your unpaid invoices and protects you against nonpayment. We provide the fastest cash turnaround in the industry, offer ongoing account management, and specialize in several different industries. Get started today to see what steady cash flow can do for your business growth.

Our Process

STEP 1

Apply

Complete form & become a Riviera client

STEP 2

Service

You deliver your products or services

STEP 3

Send

Send your invoices to Riviera Finance